Smart Contracts Explained

Smart contracts are pieces of computer codes that codify the business logic. They can help in automizing and enforcing legal obligations drawn out in an agreement. This article explains the concept of smart contracts, their usage, and future potentials.

What are Smart Contracts?

In 1996, a legal scholar, computer scientist, and cryptographer named Nick Szabo used the term smart contracts for the first time. He proposed the idea to use a distributed ledger to store traditional contracts more securely and transparently. More so, the idea was to make the process free of intermediaries.

Smart contracts are just like any contract we have for businesses, rental agreements, etc., however, the only difference being they are completely digital. The contracts are converted to computer codes, stored, and replicated on the system, and supervised by a network of computers running on the blockchain technology.

How Smart Contracts Work?

Nick Szabo explained how self-executing or smart contracts could be delivered through efficient use of secure computation, digital signatures, and cryptography. He believed in the potential of contracts that can be created and executed digitally. Smart contracts can be used to exchange money, property, or anything of value in a more transparent or hassle-free way, compared with a traditional contract – all the while avoiding the need for a middleman.

Ordinarily, you go to a lawyer or government institution to prepare a document. You pay the authorities and wait until the document is ready. Whereas smart contracts work differently and can be compared to a vending machine. For instance, you drop the information and some cryptocurrency into a vending machine (i.e., ledger), and your escrow, rental contract, or any other document drops into your account. Moreover, smart contracts not only define rules and penalties around an agreement but also automatically enforces those obligations.

How Do Smart Contracts Work in Blockchain?

If two or more participants decide to use a common blockchain platform and agree on business logic or set of rules, they can create a smart contract on the blockchain without any human intervention.

For instance, you want to rent an apartment from Joe. You can do the dealing on the blockchain by paying in the form of cryptocurrencies (such as Bitcoin). In return, you get a receipt which is held in a virtual contract. Joe will give you a digital entry key by a specified date, and if you do not get the key on time, blockchain will release your refund.

However, if Joe sends the key before the rental date, the function will hold both the fee and the key respectively. And when the date arrives, the system will run on an “if-then” premise, which will be witnessed by hundreds of people on the blockchain, so you can expect an impeccable delivery.

If Joe sends you the key, he is sure to be paid, and if you send the payment, you will receive the key. The document on the blockchain is canceled automatically after that time, and the code cannot be changed by either of the parties without the other knowing, because all participants are simultaneously notified.

Smart contracts can be used for all kinds of situations including insurance premiums, property law, financial services, crowdfunding agreements, and legal processes. Additionally, different blockchains support smart contracts, but the biggest one is Ethereum – specifically created to support them. A special programming language called Solidity is created for Ethereum that can be used to program contracts. The language uses similar syntax as JavaScript.

Bitcoin also supports smart contracts, but the use is limited as compared to Ethereum.

Major Applications

- The government can use smart contracts to automate and manage operations such as land title recording for property transfers. They make the process efficient and transparent and reduce costs required for auditing.

- Supply chain management can be improved manifold with the help of blockchain smart contracts. For instance, it can help in tracking the inventories within the supply chain with full visibility. Furthermore, they reduce verification requirements and enhance the results of tracing fraud and thefts.

- They can also support the health care sector by storing patient’s records on a blockchain with a private key that would give access to specific individuals. Receipts of surgeries, proof of insurance, etc can also be encoded and stored on the smart contract.

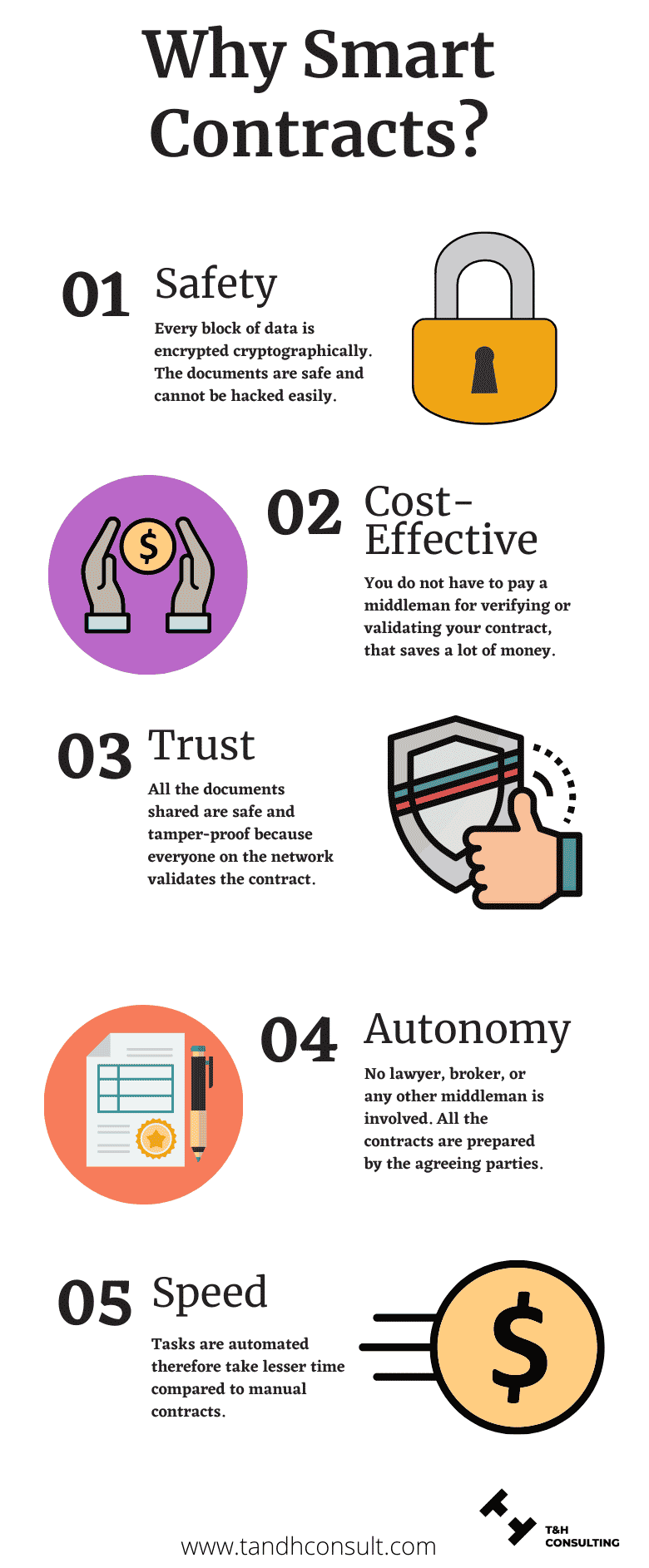

Why You Need Smart Contracts?

Here’s why you need them:

Safety – The key feature of a blockchain is that every block of data is encrypted cryptographically. The documents of the users are safe, and hacking is not easy unless the hacker is abnormally smart to crack the code.

Cost-effective – Smart contracts eliminate the requirement of an intermediary that saves a lot of money, as you do not have to pay anyone for verifying or validating the transaction.

Trust – Blockchain is highly secure and adds a layer of trust to the internet and transactions running on it. Therefore, the documents shared are secure and tamper-proof. Meaning, the output of the contract is validated by everyone on the blockchain. Therefore, no party can claim they lost the data.

Autonomy – The agreement is made by the parties involved, without any input from lawyers, brokers, or any other middleman. This also eradicates the chance of getting manipulated by a third party, since the execution is done automatically on the network.

Speed – Manually processing the documents takes plenty of time, which can be saved with the help of smart contracts as tasks are automated.

Conclusion

Conclusion

The world of business is in a process of embracing smart contracts because of their potential to solve problems in a much more transparent and secure manner. They are immutable and are distributed on a ledger. This means the output of your contract is validated by everyone on the network, and no individual can force anyone to release the funds or tamper with the codes, because other people on the network can notice the action and can invalidate it.

Smart contracts are here to make your life easier. How do you want to take advantage of this technology? Let us know in the comments below.

Learn More: